Buying a home in Queensland can be exciting, but Lenders Mortgage Insurance (LMI) adds an extra cost if you have less than a 20% deposit. Understanding what an LMI calculator is, how LMI is calculated, and the strategies to reduce it can save you thousands. In this guide, written by an expert mortgage broker, we’ll provide clear explanations, example calculations, and tips to help you find the best LMI deal for your circumstances.

Let’s dive in…

Table of Contents

LMI Calculator

What Is Lenders Mortgage Insurance (LMI) And Why Does It Matter

Lenders Mortgage Insurance (LMI) is an insurance policy that protects the lender, not the borrower. It is designed to cover the lender if a borrower defaults on a home loan. Many homebuyers confuse LMI with personal protection, but it does not cover you or your repayments.

LMI is usually required when your deposit is less than 20% of the property value. For example, if you are buying a $500,000 home with a $50,000 deposit, the lender may require LMI. The smaller your deposit, the higher the LMI premium.

Understanding LMI is important because it affects your overall home loan costs. LMI can add thousands of dollars to your loan, either as a one-off premium or included in your loan amount. This extra cost impacts your monthly repayments and the total amount you repay over time.

Key Points About LMI

- Protects the lender, not the borrower.

- Required if your deposit is less than 20%.

- Costs vary based on loan amount, LVR, property type, and lender.

- Can significantly increase your total home loan cost.

By knowing how LMI works, you can plan your deposit, compare lenders, and reduce unnecessary costs. Using a reliable LMI calculator helps you estimate premiums before committing to a loan.

Example LMI Calculations For Different Scenarios

Using our LMI calculator can help you estimate costs for your home loan. Here are some realistic examples for Queensland borrowers.

Here’s a clear side-by-side table for the three LMI scenarios in Queensland:

Scenario | Property Value | Deposit | LVR | Loan Amount | Estimated LMI |

First-Home Buyer | $800,000 | $80,000 (10%) | 90% | $720,000 | $19,000 |

Investor | $900,000 | $45,000 (5%) | 95% | $855,000 | $38,500 |

Refinancer | $1,000,000 | $200,000 (20%) | 80% | $800,000 | $0 |

Key Takeaways

- LMI increases with higher LVR and lower deposit.

- Investor loans generally have higher LMI than owner-occupier loans.

- Using an LMI calculator helps compare premiums across different lenders.

- Professional exemptions or lender discounts may reduce your LMI.

How To Get The Best LMI Deal In Queensland?

Several mortgage brokers only take into account the interest charged by various lenders. But if you want to get the whole picture of how much the loan will cost you, it is very important to keep every feature in mind.

If you wish to find the best deal, there are three things you should keep in mind:

- Find out the LMI providers, lenders, and discounts you qualify for

- Specify why you applied for a loan, what you need, and what particular features you want in your loan

- Compare the packages offered by different lenders, including the LMI premium, fees, interest rate, and other loan features.

Following this three-step approach will definitely help you secure a good deal, and it is possible to do so with an LMI calculator.

Our expert mortgage brokers can compare LMI costs between lenders for you. If you want to see your options call us on 1300 088 065 or enquire online.

Loan Approval By The Mortgage Insurer

If you are required to have mortgage insurance approval, it can be challenging to qualify for a loan.

First of all, when it comes to evaluating the 90% or 95% LVR home loan, you could struggle to find a lender who is willing to approve it. This can make the insurance approval process more difficult.

However, speak to our team about different ways you can still get the approval.

Your loan application is either accepted or rejected based on the following 2 factors:

- Passing the credit scoring criteria, and

- Meeting the genuine savings requirements.

There are a few lenders mortgage insurers in Australia, and our team of mortgage experts can help if your loan has been declined. Get in touch, or call on 1300 088 065 to discuss your options.

Read More: Home Loan Declined? 26 ways to turn your approval around.

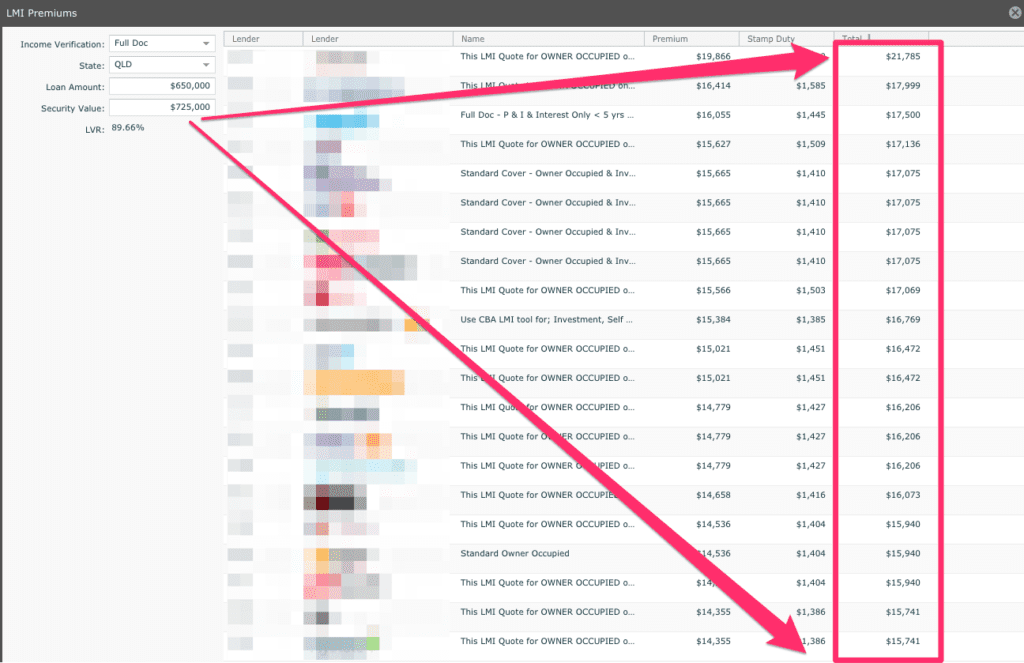

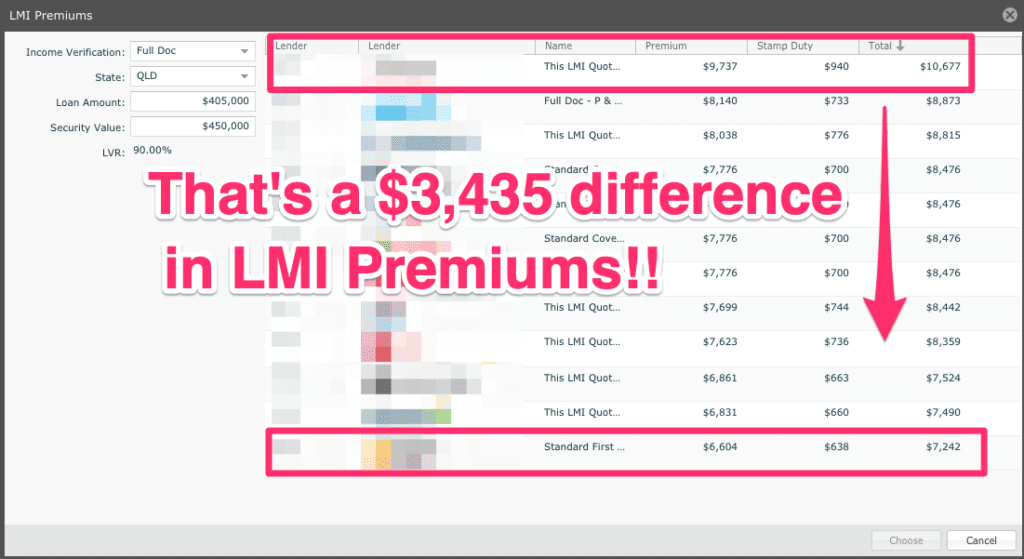

By using the LMI calculator, you can easily find out which lender offers the cheapest mortgage insurance. The criteria for cheap LMI are different in every case.

If, for example, Adelaide bank LMI is cheaper for you, it doesn’t mean it will be cheaper for your friend as well. But with the help of an LMI calculator, you can definitely find out what is a suitable option for you.

Refinancers, investors, first home buyers, and upgrades can easily get an LMI discount from various lenders. It is important to seek advice from a professional broker, as they can help you secure good LMI discounts.

Home Loan With No LMI In QLD

Getting an LMI discount is difficult as it often comes with strict qualification criteria. But the good news is that a home loan with a very low-interest rate can still qualify for this discount.

If you are a doctor by profession, you can borrow up to 100%of the property price while avoiding LMI costs at the same time.

Some professions that sometimes benefit from waived LMI include:

- Barristers

- Solicitors

- Lawyers

- Surveyor

- Geologist

- Geophysicist

- Auditors

- Actuaries

- Finance Managers

- Accountants

Read More: How to get no LMI at 90% LVR.

Lenders Who Use LMI

There are a number of lenders who use LMI to protect themselves from the risk of default. Banks that charge LMI are:

- Westpac bank,

- National Australia Bank,

- Mortgage Asset Services,

- MKM Capital,

- Merchant Mortgages,

- Mainstream Capital,

- Loan Ave

- La Trobe Financial,

- Homeloans Limited,

- FirstMac,

- Collins Securities,

- Citibank,

- BankWest,

- Australian Unity,

- Australian First Mortgage,

- ANZ,

- AMP,

- Adelaide Bank,

- Bank of Queensland,

- Australian Secured and Managed Mortgages,

- Suncorp Bank,

- RAMS Home loans,

- Pepper Home Loans,

- and more.

Although you may not be able to compare the LMI premium of all these banks with an LMI calculator, you can still gather information for your own comparison. Or simply consult our team to find the right loan package.

BONUS: Tips To Reduce Your LMI Costs

Lenders Mortgage Insurance (LMI) can add thousands to your home loan. The good news is, there are ways to reduce or even avoid it. Here are practical tips for Queensland borrowers:

- Increase your deposit – The simplest way to reduce LMI is by saving more. Deposits closer to 20% lower or eliminate premiums.

- Choose lenders offering LMI discounts – Some lenders provide discounted premiums or special offers for first-home buyers and refinancers.

- Professional exemptions – Certain professions, such as doctors, lawyers, and finance managers, may qualify to borrow up to 100% without LMI.

- Combine loans with family members – Pooling resources with a spouse or parent can boost your deposit and reduce LVR, lowering LMI costs.

- Refinance strategically – If you already have equity in your property, refinancing can reduce or remove LMI on new loans.

- Use a reliable LMI calculator – Compare multiple lenders and scenarios to identify the lowest LMI options before committing.

Following these strategies can save you thousands and make your Queensland home loan more affordable.

LMI Calculator QLD Frequently Asked Questions

Can I avoid paying LMI with less than 20% deposit?

Sometimes. Certain lenders may waive LMI for specific professions or low-risk borrowers such as doctors, lawyers, accountants, and engineers.

How is LMI calculated?

LMI depends on your loan amount, loan-to-value ratio (LVR), property type, and the lender’s premium rates.

Do all lenders charge the same LMI?

No. LMI premiums vary between lenders, so it’s important to compare options before choosing a loan.

Can investors get LMI discounts?

Yes. Some lenders offer reduced premiums for investment loans, refinancers, or multiple property owners.

Does LMI cover me if I default on my loan?

No. LMI protects the lender, not the borrower, in case of default.

Are there professions that can borrow 100% without LMI?

Yes. Certain professions, such as doctors, lawyers, and finance managers, may qualify for waived LMI.

How much can I borrow without paying LMI?

You can usually borrow up to 80% of the property value without needing LMI.

How to avoid LMI?

Increase your deposit, choose lenders offering discounts, or qualify for professional exemptions to reduce or avoid LMI.

Do you pay LMI upfront?

LMI can be paid upfront or added to your home loan, depending on lender preference.

How accurate are LMI calculators?

LMI calculators provide estimates; actual premiums vary by lender, loan amount, LVR, and property type.

Want To See If You Qualify For Discounted LMI?

We work with lenders that provide LMI discounts and even waive LMI for certain professions.

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one person operations, we have an entire team of experts dedicated to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

More Resources For Home Buyers

- First Home Buyers Guide from start to finish

- How to Buy a House (Step-By-Step Case Study)

- Using your Superannuation to build your deposit: The Complete Guide to the First Home Super Saver Scheme

- How to save for a house deposit (fast)

- Build a House in Brisbane-the Definitive Guide

The information on this page is general in nature and should not be considered advice. Before you act on this information, you must seek independent legal and financial advice.

Start again

Start again