Positive Credit Reporting (also called Comprehensive Credit Reporting or CCR) gives lenders a more complete picture of your credit history, including on-time repayments, current and closed accounts, and defaults. Unlike the old negative reporting system, CCR can improve your borrowing potential and help first-time homebuyers or those with short credit histories demonstrate reliability. Understanding how CCR works, what information it collects, and how to manage your credit report is essential for securing a home loan in Australia.

This guide, written by an expert mortgage broker will explain everything you need to know about CCR.

Quick Summary

- Introduced on 1 July 2018 for big banks

- Provides a more comprehensive view of an individual’s credit history

- Includes information on current accounts, repayment history, and closed accounts

- Affects home loan applications by giving lenders more detailed information

- Can benefit borrowers with good repayment habits

- May balance out past mistakes with recent good behaviour

- Allows for a more nuanced assessment of creditworthiness

Table of Contents

What Did Credit Reports Previously Show?

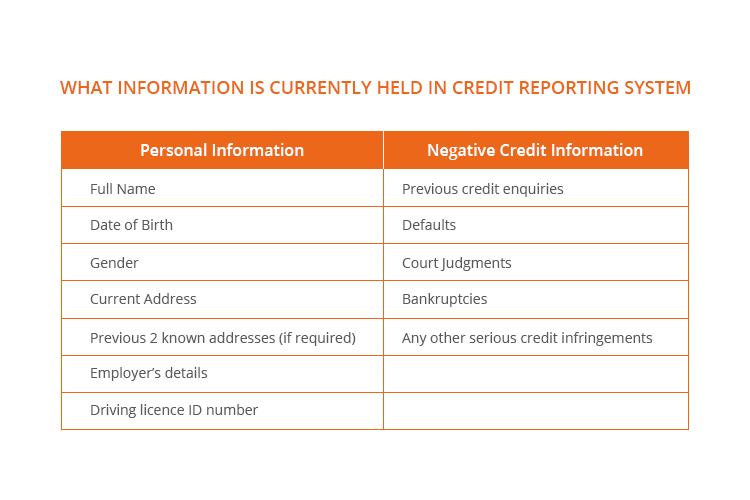

Before 1 July 2018, banks used negative credit reporting and based their credit reporting assessment on whether or not you had any negative information on your credit file. The level of information was pretty basic—it recorded things like account numbers and included details of any overdue debts, defaults, bankruptcies and court judgments against you. It also included the type of credit application you made but did not record whether you were approved or declined.

Types Of Data Reported Under Comprehensive Credit Reporting (CCR)

Comprehensive Credit Reporting provides lenders with a much more complete picture of your credit history than the old negative reporting system. The types of information included can be grouped into the following categories:

1. Personal Information

- Full name, date of birth, and gender

- Current and previous addresses

- Driver’s licence or identification numbers

- Employment details (current employer, job title)

2. Credit Accounts

- Current accounts: All active credit accounts including home loans, personal loans, credit cards, car loans, and store cards

- Closed accounts: Details of accounts you have closed within the reporting period

- Account type and credit limit: The type of credit (e.g., mortgage, credit card, personal loan) and approved credit limits

3. Repayment History

- Payment performance: Shows whether you have made repayments on time over the last 24 months

- Missed or late payments: Records any late payments and how often they occur

- Default notices: Includes notices issued by lenders for overdue debts

- Discharged defaults: Shows if previously unpaid debts have been resolved

4. Credit Applications

- Applications made: The type and date of any credit applications you have submitted

- Outcome of applications: Whether your application was approved or declined (available only in CCR, not under negative reporting)

5. Public Record Information

- Bankruptcies and court judgments (if any)

- Other public records relevant to your creditworthiness

6. Account Status & Activity

- Current balance on credit accounts

- Amounts overdue or in arrears

- Limits on accounts and any changes over time

Key Takeaway: CCR gives lenders a holistic view of your financial behaviour, helping them assess your reliability and overall creditworthiness beyond just defaults or late payments.

What Does Positive Credit Reporting Show?

Positive Credit Reporting, also known as Comprehensive Credit Reporting (CCR), gives lenders much more information, including a complete history and current snapshot of your credit cards and bank accounts within Australia.

Positive credit reports now include information about your current accounts, which accounts have been opened (and closed), any payments on default notices, and, most importantly, how well you meet your ongoing repayments.

Who Can See Your CCR Data & How To Manage Privacy

Comprehensive Credit Reporting (CCR) gives lenders a detailed view of your credit history, which helps them assess your borrowing risk. At the same time, it’s important to understand who can access this data and how you can manage your privacy.

Who Can Access Your CCR Data

- Lenders with Consent: Only banks, credit unions, or other credit providers can access your CCR data, and only if you give permission when applying for credit.

- No Automatic Sharing: Your credit report is not automatically shared between lenders without your consent. Each credit application triggers a separate consent request.

How to Manage Your CCR Privacy

- Limiting Data Sharing: You can ask your credit provider to limit the reporting of certain account types, though you cannot fully opt-out of CCR for existing accounts.

- Future Accounts: For new accounts, you may request that some positive data is not reported. Keep in mind that this could affect how lenders view your borrowing capacity.

- Check Your Rights: The Office of the Australian Information Commissioner (OAIC) offers guidance on accessing, correcting, or restricting your credit information.

- Practical Tip: Review your credit provider’s privacy policy and speak with them if you want to control which information is reported.

Key Takeaway: In Australia, your CCR data is only visible to lenders who have your consent. While full opt-out isn’t possible, you have control over how and when your data is shared, helping you maintain privacy while still benefiting from a comprehensive credit profile.

How does Comprehensive Credit Reporting Affect Applying For A Home Loan?

When you apply for a home loan using the Positive Credit Reporting system, banks will now have access to see if you have been repaying your personal loans, car loans, credit cards or home loans over the past 2 years. This also includes any accounts that you have also closed during this time.

Under the old negative reporting system, your credit report wouldn’t show any information about how well you’ve been paying off your home loan, personal loan or credit card. Now the banks will have a much more comprehensive picture of your personal repayment history.

Positive credit reports do not contain the most recent 14 days of information, so it is likely they are still going to want to get copies of your home loan and bank statements.

Impact On First-Time Homebuyers

Positive Credit Reporting can be particularly beneficial for first-time homebuyers in Australia. Previously, those without an extensive credit history might have struggled to secure a home loan. Now, with CCR, lenders have access to a more comprehensive picture of an individual’s financial behaviour.

For example, a young professional who has been consistently paying rent and utilities on time, but hasn’t had a credit card or personal loan, can now demonstrate their reliability to lenders. This expanded credit profile can potentially improve their chances of securing a home loan.

However, it’s important to note that while CCR provides more information, first-time homebuyers should still focus on saving for a deposit and demonstrating stable income. Lenders will consider these factors alongside the credit report when assessing a home loan application.

How CCR Affects Interest Rates and Borrowing Power

Comprehensive Credit Reporting (CCR) doesn’t just show lenders whether you’ve missed payments—it gives them a complete picture of your financial behaviour. This deeper insight can directly impact the interest rates you’re offered and your borrowing capacity when applying for a home loan. Understanding this connection can help you take actionable steps to improve your loan terms.

Here are some ways positive credit reporting can affect your interest rates and borrowing power:

- Improved Interest Rates: Borrowers with a strong record of on-time repayments may qualify for lower interest rates. For example, a young professional with no defaults and a consistent repayment history could be offered 0.2–0.5% lower interest than someone with similar income but a shorter or mixed credit history.

- Higher Borrowing Limits: Lenders may approve a larger loan if your CCR shows stable repayment behaviour across multiple accounts. For instance, someone with a spotless 24-month repayment record on a personal loan and credit card could secure a home loan that’s 5–10% higher than someone with limited credit history.

- Better Negotiating Power: Positive data allows borrowers to negotiate more favourable loan features, such as offset accounts, redraw facilities, or flexible repayment options, because lenders perceive lower risk.

Key Takeaway: Maintaining a clean and consistent credit history under CCR can translate directly into tangible financial benefits—lower interest rates, higher borrowing limits, and more flexibility when structuring your home loan.

Summary Table: How CCR Impacts Loan Assessment.

Borrower | Credit History (24 months) | CCR Impact | Hypothetical Home Loan Outcome |

Jane | All payments on time | Positive credit behaviour recognised | Pre-approved for $912,563 loan at 5.2% interest |

Mark | One missed payment 6 months ago | Minor impact; pattern still positive | Pre-approved for $880,000 loan at 5.5% interest |

Lisa | Multiple missed payments | Negative credit behaviour highlighted | Conditional approval for $750,000 loan at 6.2% interest |

Tom | Short credit history, all on-time | CCR shows reliability despite short history | Pre-approved for $800,000 loan at 5.4% interest |

Note: These figures are for illustrative purposes only. To find your true borrowing capacity, speak with a mortgage broker today.

How CCR Benefits Different Borrower Types

Young Professionals with Limited Credit

- Scenario: James, 28, recently started his career and has a credit card with on-time repayments and a small personal loan.

- Impact: CCR highlights his positive repayment pattern, demonstrating responsible money management.

- Potential Benefit: Can access competitive personal loan or credit card offers, and potentially secure pre-approval for a home loan sooner.

Renters Looking to Transition to Homeownership

- Scenario: Sarah, 32, has been renting for years and paying rent and utilities reliably but has minimal other credit history.

- Impact: CCR allows lenders to consider rent and utility payment data where available (through some rent reporting services), supplementing limited formal credit.

- Potential Benefit: May improve eligibility for a home loan or reduce perceived risk, even without a long credit record.

Borrowers Recovering from Past Defaults

- Scenario: Liam, 40, had a single default 5 years ago but has since maintained on-time payments for all loans and credit cards.

- Impact: CCR provides a more balanced view of his current financial behaviour.

- Potential Benefit: Past isolated defaults are weighed against consistent recent repayments, improving his chances of securing loans at standard rates.

Positives Of Positive Credit Reporting

- All your hard work making repayments on time will be recognised: If you’ve always kept your credit card or personal loan repayments on time, the banks will know you’re a good candidate for a home loan.

- Your good conduct can balance out a few mistakes in the past. If you moved house 4 years ago and got a phone bill default but have since kept perfect conduct on all of your accounts, the good behaviour will balance out the negative of having a default on your credit file.

- Having a short credit history will be a thing of the past: Some first homeowners get a home loan before they get a credit card. Previously this might have impacted them as they didn’t have a long credit history. Now, Positive Credit Reporting will give the banks more data.

- Your credit score won’t be significantly impacted by one bad event like a missed payment: As positive credit reports your last 24 months of payment history, one lone missed payment can be explained. As long as there isn’t a general pattern of credit stress, the banks will still be able to consider you a creditworthy borrower.

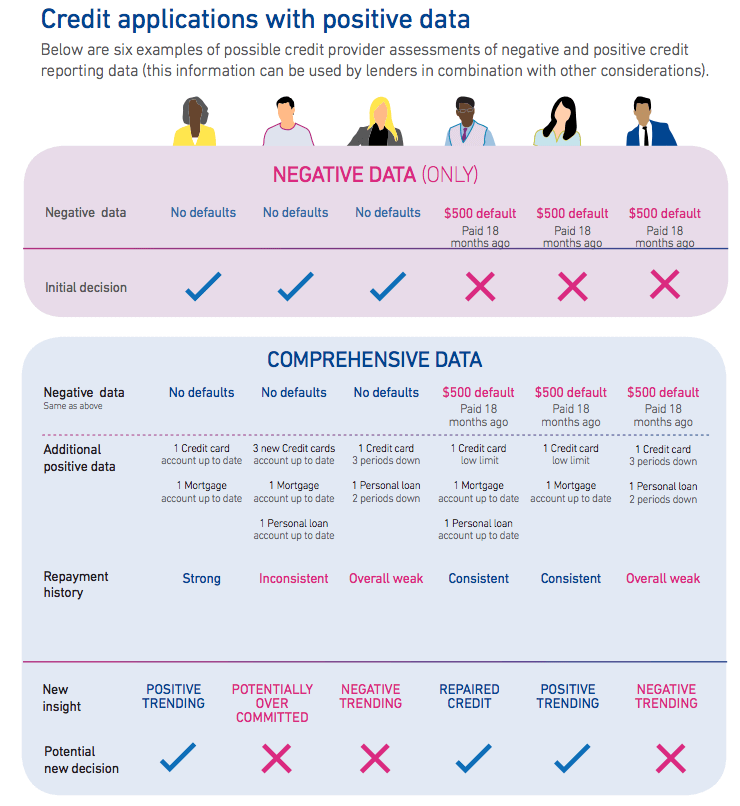

What is an example of how positive data will help loan applications?

Here are a few examples of how a bank or lender would look at and assess people with negative and positive credit reporting.

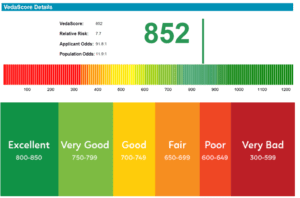

Where Can I Get A Copy Of My Credit Report?

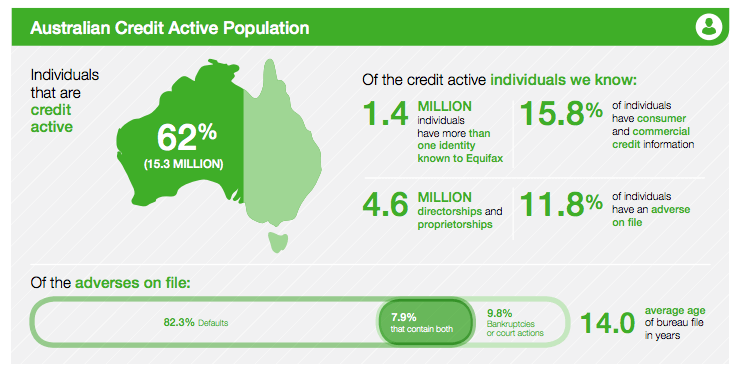

Did you know over 65% of Australians have never checked their credit score?

Knowing your credit score and how it may impact your finances in the future is critical. A bad credit score could stop your plans to buy property before they even start!

We recommend checking your credit score at least once a year. This can be done for free using MyCreditFile, which is run by Equifax, or by using illion (formerly known as Dun and Bradstreet).

At Hunter Galloway, we can also assist with getting a copy of your credit report. If you would like a copy, call us on 1300 088 065 or get in touch here.

Your credit report will show your complete view of your credit history in Australia.

What Stuff Should I Check On My Credit File?

The banks are required by law to ensure the information on your credit file is up to date and accurate. However, errors can sometimes happen—information might not be passed on, or it can just be wrong.

In short, it’s worth double-checking the following information on your credit file:

- Loans and Debts: Make sure these are your debts. We’ve seen situations where people had loans they did not know about appearing on their credit files. Once you are certain the debts are yours, check that the amount is correct and that there aren’t any duplicates.

- Defaults: You will see a default on your credit file if your repayments are more than 60 days late and the amount due is over $150. Check that these details are correct and you did receive the notices listed. If you have settled the overdue amount, make sure it is showing as ‘paid.

- Your personal information: Check that your name, gender, date of birth, current address, driver’s licence number and current employer are all correct

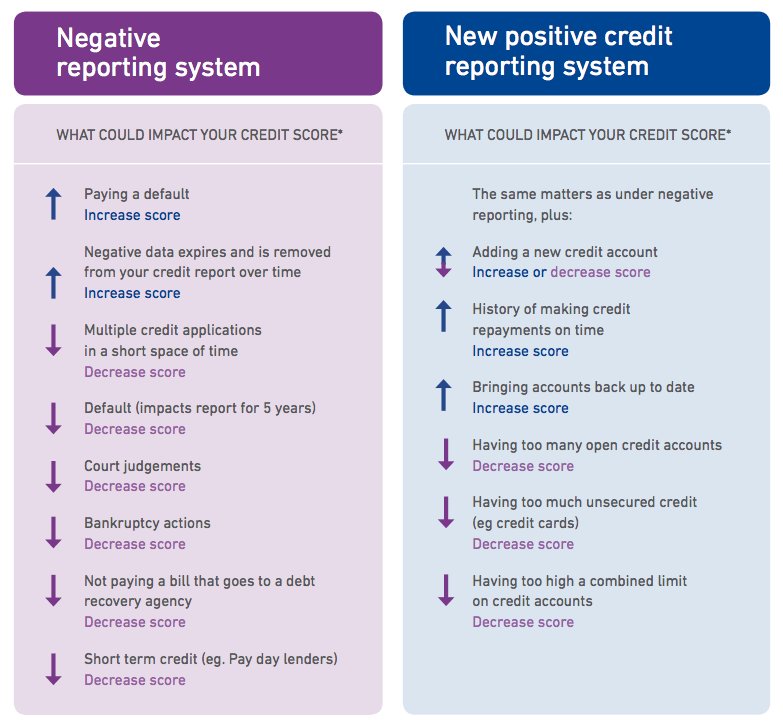

What Sorts Of Things Impact My Credit Score?

As you have seen, in the old negative reporting system, something as simple as having multiple credit applications in a short space of time or lots of short-term credit could decrease your score.

In the new positive credit reporting system keeping your accounts up to date and having a history of making your credit repayments on time can help increase your credit score.

What Doesn't Impact My Credit Score?

The following won’t impact your credit score:

- A late phone bill won’t impact you unless you go into default.

- Checking your credit score won’t impact it negatively as this is considered a ‘soft enquiry.’

- Your income does not affect your credit score. Your credit score shows how well you manage money rather than how much you earn.

- Investments. Your investments or savings do not have an impact on your credit score.

- Personal information like your gender, race or religion does not affect your credit score.

- Getting divorced might not directly affect your credit score. But sometimes, after a divorce, accounts and loans can be split, affecting your credit score.

- Paying with a debit card won’t affect your credit score because when you pay using a debit card, you are using the money you already have in your account and not borrowing anything. Paying with a credit card is essentially borrowing, so that will affect your credit score.

- Getting a pay rise (or pay cut) or changing jobs may or may not impact your credit score.

Things that affect your credit score are simple and complex at the same time.

According to Experian, “A score may go up or down because of new information, but not always. For instance, if you already have a very low credit score, a new default may not lower your score any further. Similarly, a default will stay on your credit report for five years even once you pay it off, and should there be other defaults on your file, your score may not necessarily increase. Likewise, if you already have a very high credit score, continuing to make your payments on time may not make your score go any higher. It’s important to note that there is no quick way to fix a credit score – repairing bad credit takes time.”

BONUS: Regulatory Framework for Comprehensive Credit Reporting (CCR) In Australia

Comprehensive Credit Reporting (CCR) is governed by a combination of legislation, regulations, and industry standards to ensure transparency, fairness, and consumer protection. Key regulatory bodies and their roles include:

Australian Securities and Investments Commission (ASIC)

- Responsible Lending Obligations: Under the National Consumer Credit Protection Act 2009, ASIC mandates that credit licensees must not enter into a credit contract with a consumer if the contract is unsuitable. This includes making reasonable inquiries about a consumer’s financial situation and taking steps to verify it.

- Guidance on Repayment History Information: ASIC has provided guidance on the use of repayment history information, emphasizing that past repayment difficulties do not necessarily mean that a new credit product will be unsuitable for the consumer in all cases.

- Consumer Data Right (CDR) Rules: The ACCC oversees the Consumer Data Right, which includes rules for the sharing of credit information. These rules facilitate greater consumer control over their data while ensuring that sensitive information, such as financial hardship arrangements, is protected.

- Principles of Reciprocity and Data Exchange (PRDE): The ACCC has re-authorized the PRDE, which sets out rules and standards for participating credit providers and credit reporting bodies to follow when contributing and accessing consumers’ comprehensive credit information.

How Can I Increase My Credit Score?

- Pay your bills on time. The easiest way to implement this is to set up all your bills on a direct debit so you always remember to pay them.

- Keep track of your credit file. There are several services that will SMS and email you whenever a company inquires on your credit file. This service is only getting increasingly important as cybercrime increases and will allow you to catch it early. As mentioned above, you can use Illion or Equifax.

- Dispute any inaccuracies on your credit file. There are countless stories where people have had information listed on their credit file that wasn’t theirs. This usually happens if you have a common name, and we would need to rectify it straight away.

- Limit the number of credit inquiries. Try to avoid having a hyperactive credit file at all costs, e.g. applying for too much credit in a short period. As a rule of thumb, it is best to limit your activities and inquiries to at most five a year. Remember, Telco and utilities also count.

- Limit the number of banks you bank with. We suggest having no more than two providers, and ideally one. Having many banks makes it harder to manage your money. This is because the more institutions you have, the greater the chance of missing a payment and not having sufficient money to cover a direct debit.

- Remove unwarranted defaults. The first thing to do is get a copy of your credit file and double-check it. It’s common for defaults to be listed without you even knowing. If this has happened to you, there is no need to despair. It’s likely the provider didn’t follow the required protocol of contacting you and ensuring you had a chance to remedy the payment. In cases like these, there are countless credit repair lawyers who’d be able to rectify this wrong.

- Don’t change your job or location frequently. Most people don’t know this, but the more you move, the lower your credit score. Lenders want to be able to find people they lend money to, so the more you move, the higher the chance of it being harder for the lender to find you if things go belly-up. So aim to stay in the same location and job for at least 24 months at a time.

Frequently Asked Questions (FAQs)

What is Positive Credit Reporting (CCR)?

Positive Credit Reporting, also known as Comprehensive Credit Reporting, is a system that provides lenders with a detailed view of your credit history, including your repayment behaviour, current accounts, and closed accounts. It helps lenders assess creditworthiness more accurately in Australia.

How does CCR affect my credit score?

CCR considers your repayment history over the past 24 months. Consistently paying bills, loans, and credit cards on time can improve your credit score, while repeated missed payments may lower it. Positive behaviour can also offset minor past defaults.

Can Comprehensive Credit Reporting impact my loan pre-approval?

Yes. Lenders can access CCR data (with your consent) during pre-approval to evaluate your borrowing capacity. Good Credit history may increase your borrowing limit and improve the likelihood of pre-approval for home loans, personal loans, and credit cards.

Who can see my credit report data?

Only lenders or credit providers that you have explicitly given consent to can access your CCR data. Your credit report is not public, and access is strictly controlled under Australian privacy laws.

How is my credit score calculated?

CCR does not produce a separate “score,” but it contributes to your overall credit score by reporting detailed repayment behaviour. The score considers timely repayments, account activity, and any defaults over the past two years.

How do I dispute errors on my credit report?

If you notice inaccuracies, you can contact the credit reporting agency (Equifax or illion) to dispute the error. They are legally required to investigate and correct mistakes within a reasonable timeframe. Always keep records of your correspondence.

Does checking my own credit report affect my credit score?

No. Checking your own report is considered a “soft enquiry” and does not negatively impact your credit score. Only credit applications by lenders (“hard enquiries”) can affect your score.

Can positive credit reporting improve my interest rates or borrowing limits?

Yes. Lenders may offer lower interest rates (0.1–0.3% lower) or increase borrowing limits by 5–15% for borrowers with a positive 24-month repayment history. CCR gives lenders confidence in your repayment reliability.

Summary And Next Steps

Positive Credit Reporting is here to stay. With static credit score, if you had missed a payment on your credit card or personal loan, all you needed to do was close it down, and the problem was gone.

Now there’s no escape because the record stays on your credit file for up to two years. This means now it is even more important to pay your bills on time and in full.

Talk to our Mortgage Brokers to get a free copy of your credit report. We will also review it for you and see what your home loan options are. So, call us on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again